The Chancellor presented his final spring budget before the election, emphasizing reforms designed to streamline the tax system, promote fairness, adapt to economic changes, and bolster public finances. As in past budgets, there are several consultations and additional details forthcoming in the following weeks.

SPRING BUDGET IMPACT ON BUSINESSES

Full Deduction for Leased Assets

Within the Spring Budget, The Chancellor proposed implementing full expensing tax relief for leased assets, aiming to enhance business efficiency by facilitating the leasing of assets to improve productivity through acquiring the latest, cleanest, and most efficient plant and machinery. The timeline for the relief’s commencement remains undisclosed, pending the publication of draft legislation.

UK Independent Film Tax Credit

Introduced at the Spring Budget 2024, the UK Independent Film Tax Credit (IFTC) allows eligible films to claim an enhanced Audio-Visual Expenditure Credit (AVEC) at a rate of 53% on qualifying expenditure. To be eligible, productions must have commenced principal photography on or after April 1, 2024, with claims acceptable from April 1, 2025, onwards for expenses incurred from that date.

Theatre Tax Relief

Legislation will be introduced in the Spring Finance Bill 2024 to establish permanent headline rates of relief for Theatre Tax Relief, Orchestra Relief, and Museums and Galleries Exhibition Tax Relief at 40%/45% (for non-touring/touring and orchestral productions, respectively), effective from April 1, 2025.

Extension of Recovery Loan Scheme From The Spring Budget

The Recovery Loan Scheme will be extended and renamed the Growth Guarantee Scheme, maintaining its existing terms and offering a 70% guarantee to lenders on finance of up to £2 million to smaller businesses.

Spring Budget 2024 Changes to VAT Thresholds

Effective April 1, 2024, the taxable turnover threshold for VAT registration will increase from £85,000 to £90,000, while the threshold for deregistration will rise from £83,000 to £88,000.

Abolition of Furnished Holiday Lettings (FHL) Regime

The FHL tax regime will be abolished, removing tax advantages for landlords who let out short-term furnished holiday properties compared to those leasing residential properties to long-term tenants, effective April 2025.

SPRING BUDGET IMPACT ON INDIVIDUALS

Income Tax Adjustments

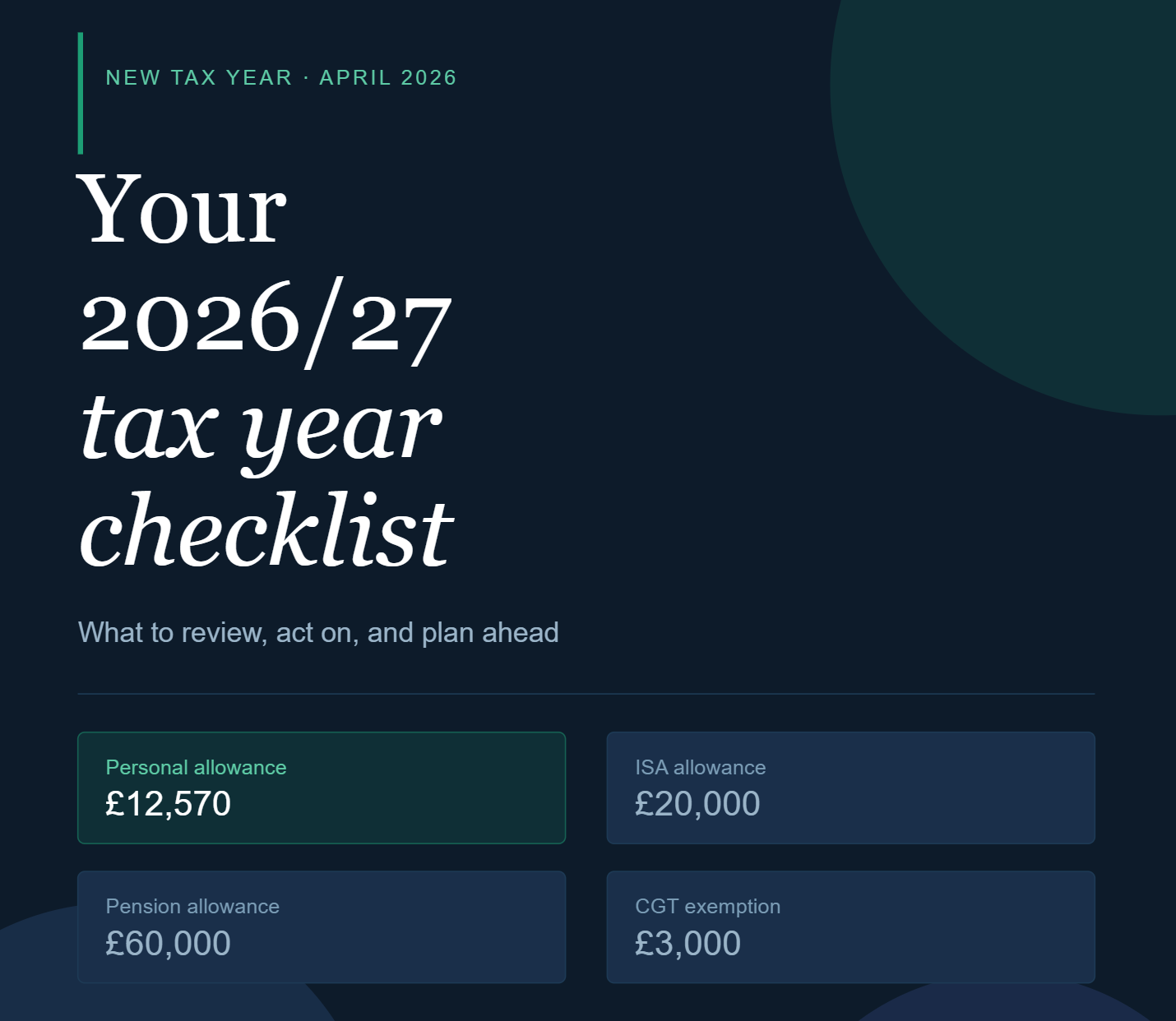

Personal tax thresholds, including personal allowance, basic, and higher-rate thresholds for income tax, will remain frozen until April 2028 at current levels (£12,570 and £50,270). The additional rate threshold was reduced to £125,140 from £150,000 starting April 6, 2023.

National Insurance Changes

Legislation will be introduced to reduce the main rate of primary Class 1 National Insurance contributions to 8% from 10% from April 6, 2024. For self-employed individuals, the main rate of Class 4 National Insurance contributions will decrease from 8% to 6% from the same date.

Capital Gains Tax Adjustments

The annual exemption amount for capital gains tax will decrease from £6,000 to £3,000 starting April 2024. Higher rate taxpayers will see their CGT rate on gains from disposals of residential properties reduced to 24% from the same date.

Replacement of Non-dom Status

The remittance basis of taxation for non-UK domiciled individuals will be replaced with a simpler residence-based regime effective April 6, 2025. Additionally, plans are underway to transition to a residence-based regime for inheritance tax.

Other Adjustments From Spring Budget

- High Income Child Benefit Charge threshold will increase to £60,000, with a tapered charge between £60,000 and £80,000 starting from the 2024-25 tax year.

- Introduction of a new UK ISA with an additional allowance of £5,000, alongside the existing annual allowance of £20,000, following a consultation period from March 6, 2024, to June 6, 2024.

- Stamp Duty Land Tax (SDLT) Relief for Multiple Dwellings to be Withdrawn From June 1, 2024, purchasers of residential property in England and Northern Ireland acquiring more than one dwelling in a single or linked transactions will not be eligible for Multiple Dwellings Relief.

Additional Resources for HMRC

The government is investing further in HMRC‘s capacity to tackle tax non-compliance, including strengthening measures against promoters of tax avoidance and enhancing taxpayer protections. Consultations are ongoing regarding options to bolster the regulatory framework in the tax advice market and the potential requirement for tax advisers to register with HMRC to interact on behalf of clients.

KEY TAX RATES FROM THE SPRING BUDGET

| Income tax rates: England, Wales & Northern Ireland (non-dividend income) |

2024/25 | 2023/24 |

| 0% starting rate for savings only | Up to £5,000 | Up to £5,000 |

| 0% on personal allowance (subject to any clawback of PA) | £0 – £12,570 | £0 – £12,570 |

| 20% basic rate tax | £12,571 – £50,270 | £12,571 – £50,270 |

| 40% higher rate tax | £50,271 – £125.140 | £50,271 – £125.140 |

| 45% additional rate tax | Above £125,140 | Above £125,140 |

| Scottish rates of income tax (non-dividend income) | ||

| 0% on personal allowance (subject to any clawback of PA) | £0 – £12,570 | £0 – £12,570 |

| 19% starting rate | £12,571 – £14,876 | £12,571 – £14,732 |

| 20% basic rate tax | £14,877 – £26,561 | £14,733 – £25,688 |

| 21% intermediate rate tax | £26,562 – £43,662 | £25,689 – £43,662 |

| 42% higher rate tax | £43,663 – £75,000 | £43,663 – £125,140 |

| 45% advanced rate | £75,001 – £125,140 | n/a |

| 48% top rate (47% for 2023-24) | Above £125,140 | Above £125,140 |

| National insurance | 2024/25 | 2023/24 |

| Lower earnings limit, primary class 1 (per week) | £123 | £123 |

| Upper earnings limit (UEL), primary class 1 (per week) | £967 | £967 |

| Primary threshold (PT) (per week) | £242

|

£242

|

| Secondary threshold (per week) | £175 | £175 |

| Employment allowance (per year/employer) | £5,000 | £5,000 |

| Employee’s primary class 1 rate between PT and UEL

From 6 April 2023 to 5 January 2024 From 6 January 2024 to 5 April 2024 |

8% |

12% 10% |

| Employee’s primary class 1 rate above upper earnings limit | 2%

|

2%

|

| Married woman’s reduced rate between PT and UEL

From 6 April 2023 to 5 January 2024 From 6 January 2024 to 5 April 2024 |

1.85% |

5.85% 3.85% |

| Married woman’s rate above upper earnings limit | 2% | 2% |

| Employer’s secondary class 1 rate above secondary threshold | 13.8% | 13.8% |

| Class 2 small profits threshold (per year) | £6,725 | £6,725 |

| Class 2 lower profits threshold (per year) | n/a | 12,570 |

| Class 2 small profit threshold (voluntary- per week) | £3.45 | £3.45 |

| Class 2 rate (per week where profits are above lower profits limit threshold | £0 | £3.45

|

| Class 3 voluntary rate (per week) | £17.45 | £17.45 |

| Class 4 lower profits limit | £12,570 | £12,570 |

| Class 4 upper profits limit | £50,270 | £50,270 |

| Class 4 rate between lower profits limit and upper profits limit | 6% | 9% |

| Class 4 rate above upper profits limit | 2% | 2% |

| Class 1A/1B NIC | 13.8% | 13.8% |